The European Union’s Carbon Border Adjustment Mechanism (EU CBAM) underscores the importance of data, carbon accounting, and strategic trade policy for industrial innovation. These tools determine what gets measured, rewarded, and whether cleaner production in the United States (US) can compete globally. This high-level explainer captures what the EU CBAM is, how it works, and its implications for US industry and policy. It is also an example of why trade will be an important focus as the Initiative develops its 2026 Federal Policy Blueprint.

What is the EU CBAM?

The EU CBAM seeks to address carbon leakage by imposing a carbon price on imports based on embedded emissions of a particular good. Embedded emissions are the direct and indirect emissions associated with the production of a product. Carbon leakage occurs when companies relocate production to countries with less stringent regulations. This can lead to imports having higher embedded carbon than domestically produced goods. EU CBAM initially applies to imports of aluminum, cement, fertilizer, hydrogen, iron and steel, and electricity. The list of covered goods is expected to expand, potentially including all products covered by the European Union Emissions Trading System (EU ETS) by 2030.

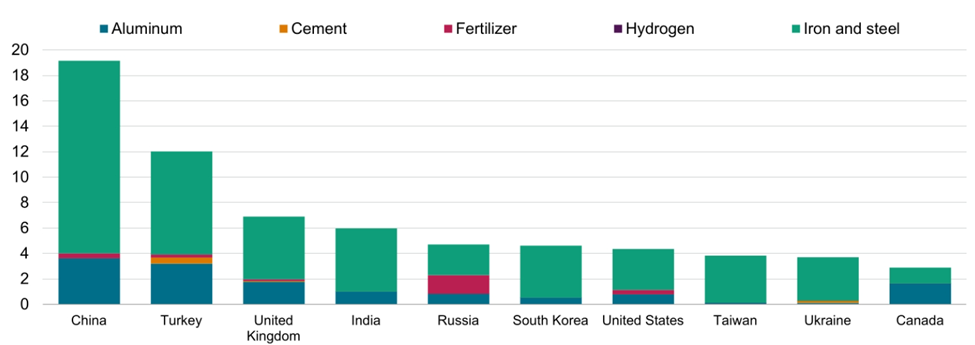

Top suppliers of goods in EU CBAM scope, 2025 ($B), as of March 16, 2026

The CBAM was introduced in 2021 as part of a broader package of proposals aimed at reducing the EU’s net greenhouse gas emissions by at least 55 percent by 2030. In 2023, these proposals were approved and adopted as part of the “Fit for 55” package.

Implementation phases and CBAM calculation

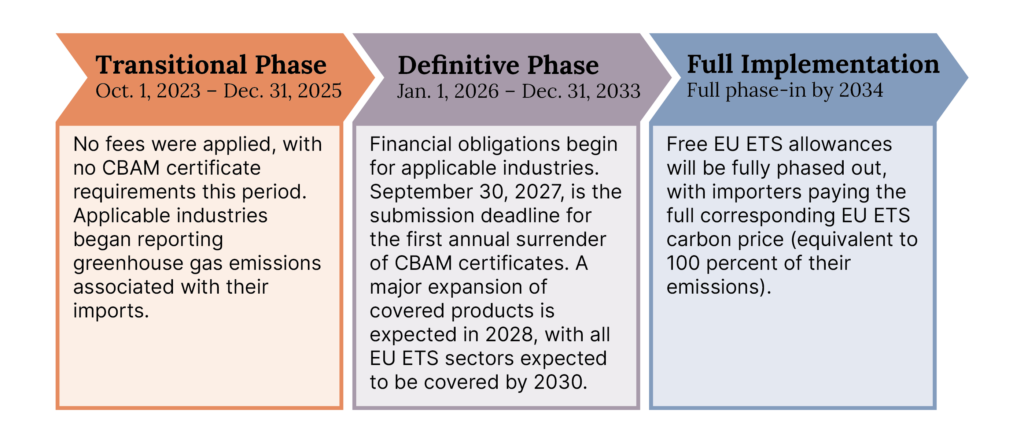

Beginning January 1, 2026, EU CBAM entered the definitive phase, the second of three phases.

During the definitive phase, applicable industries that import more than 50 metric tons of covered goods must apply for “authorized CBAM declarant” status and purchase CBAM certificates. The auction price of the EU ETS allowances determines the price of the certificates. Prices will be quarterly averages in 2026 and weekly averages beginning in 2027. On April 7, the European Commission published the first quarterly CBAM certificate for Q1 2026 at 75.36 euros.

EU ETS allowances are a key “cap-and-trade” tool in the EU’s Green Deal, designed to reduce domestic emissions in the industrial and power sectors. An allowance acts as a permit to emit one metric ton of carbon dioxide. The total number of available allowances is capped and decreases each year. Companies surrender allowances equivalent to their emissions and can also buy and trade allowances. The EU allocates free allowances to sectors that compete internationally with non-EU companies to maintain global competitiveness.

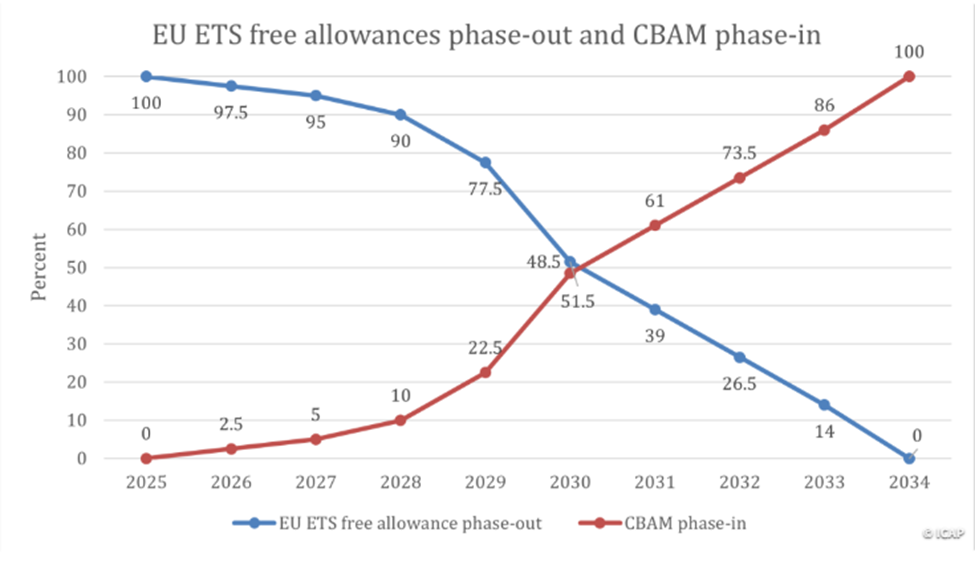

As a carbon pricing tool, EU CBAM complements the EU ETS cap-and-trade system by ensuring that both domestic and imported goods are subject to an equivalent carbon price. Similarly, the phase-in of EU CBAM between 2026 and 2034 complements the phase-out of existing free allowances under the EU ETS. By 2034, CBAM will replace the protection that certain domestic EU sectors currently receive through free ETS allowances.

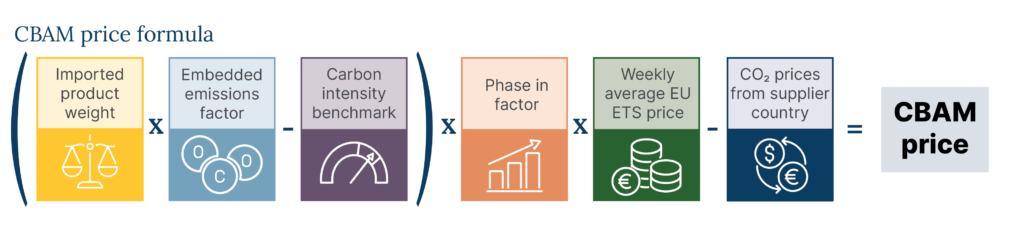

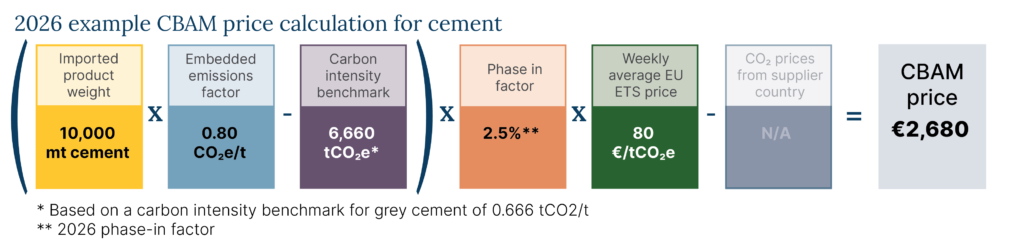

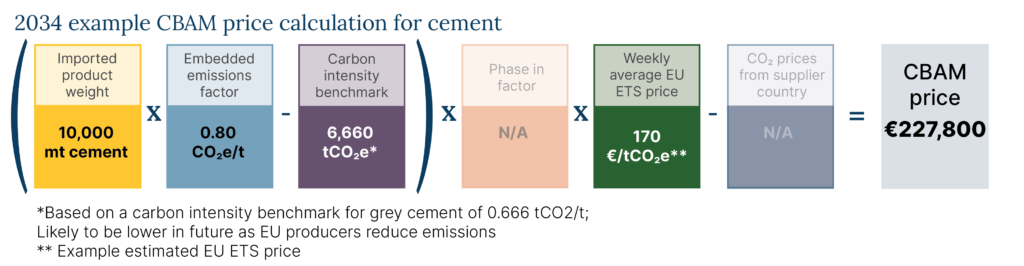

An example of a CBAM calculation based on a carbon-intensity benchmark for Portland cement (grey cement) of 0.666 tons of carbon dioxide per ton of cement (tCO2/t) is shown below for 2026 and 2034. The EU CBAM price formula includes a deduction for importing jurisdictions with their own carbon price. This box is grayed out in the 2026 and 2034 examples below to reflect current US policy conditions.

CBAM verification and default values

Facilities producing products covered under EU CBAM must undergo verification of reported embedded emissions by an accredited body in preparation for the collection of EU CBAM fees beginning in September 2027. Companies must calculate embedded emissions in accordance with the methods established in Annex IV and further specified in the Implementing Regulations adopted pursuant to Article 7(7). Companies will report 2026 emissions beginning January 1, 2027, and they must monitor emissions throughout 2026 in preparation.

When verified emissions data are not available, EU default values are applied. Default values are calculated and assigned according to the EU’s methodology rather than an individual product’s actual embedded emissions. In some cases, default values exceed a product’s actual carbon intensity, raising compliance costs, impacting competitiveness in the EU market, and underscoring the importance of reliable carbon data.

Implications for US policy

In addition to preventing carbon leakage, the EU CBAM aims to influence global trade and encourage other countries to adopt carbon pricing policies. While not enacted, several recent federal proposals related to carbon pricing and trade in the United States include the 2024 PROVE IT Act (S. 1863/ H.R. 8957), the 2025 Foreign Pollution Fee Act (S. 1325), and the 2025 Clean Competition Act (S. 3523 / H.R. 6787).

Notably, a recent Department of Energy (DOE) appropriations report included language similar to the 2024 PROVE IT Act. The National Energy Technology Lab is to conduct a study comparing the emissions intensity of certain goods produced in the US to those produced elsewhere, specifically goods covered under the EU CBAM. The Initiative will continue to monitor these developments closely.

Thank you to AJW, Inc. and the Bipartisan Policy Center for presenting on this topic during the Initiative’s January 2026 plenary.